Why is RWA Suitable for Top-tier Enterprises an Industry Upgrade Pattern?

Original Article Title: "Why is RWA Suitable for Head Enterprise an Industry Upgrade Model?"

Original Author: Yekai (Wechat/Twitter: YekaiMeta)

Will the traditional manufacturing industry really be eliminated in the Web3 wave?

No! Despite the United States' efforts over the years to move manufacturing out of China, it is easy to move a factory but extremely challenging to move an entire industrial chain.

More importantly, as Bitcoin is about to become a reserve asset in multiple countries worldwide, how can traditional industries align with Bitcoin and seize this new opportunity?

The answer is: RWA Asset Tokenization. Through the tokenization of RWA (Real World Assets), traditional enterprises can not only establish a mapping relationship with Bitcoin but also achieve cross-border financing. For top-tier enterprises, the true value of RWA lies not only in financing but also in driving the digital upgrade of the entire industry chain and asset securitization.

What are the Pain Points for Enterprises?

1. Financing Difficulty: A single manufacturing enterprise finds it challenging to bear high annualized financing costs (annualized 7 points + 1/2 point financing cost) unless it can incorporate upstream and downstream scenarios and rewards together.

2. Poor Liquidity: Traditional assets are difficult to move quickly, causing companies to miss out on market opportunities.

3. High Friction Costs: The settlement and financing costs of traditional finance remain high, hindering industrial development.

Several key points for industrial upgrading actually correspond to several pain points of traditional industries:

Financing difficulty, so start with the equity-based underlying RWA assets, similar to U.S. Treasury bonds only being private placement and primary level;

Liquidity, corresponding to industrial trading and liquidity pools, Staking the first layer of RWA assets, making liquidity from exchanges and secondary markets;

High friction costs of traditional finance require a more significant and long-term approach, with industry scenarios requiring the integration of transactions with the industry to create industry stablecoins, PayFi, and industrial DeFi, reducing industry payment settlement and fund costs for investment and financing, revitalizing industrial upgrading and liquidity, thereby promoting the stability or growth of underlying RWA asset returns, ultimately forming a positive cycle.

In this field, we are the most professional, both in terms of depth and breadth, as well as interdisciplinary.

What to do? RWA is the antidote!

The heavy asset and supply chain advantages of traditional manufacturing are naturally suited to realize industrial upgrades through RWA. The core framework of industrial upgrading includes:

• Underlying Asset Pool: From raw materials to fixed assets, distributed on-chain, dynamically priced.

• Industrial Chain Scenarios: Building tokenized transactions and liquidity pools around mining, supply chain finance, international trade, etc.

• Industrial Finance and Stablecoin: Optimizing payment, financing, and settlement efficiency through industrial stablecoins and PayFi.

• RWA Trading Platform: Ultimately forming vertical exchange platforms and liquidity support.

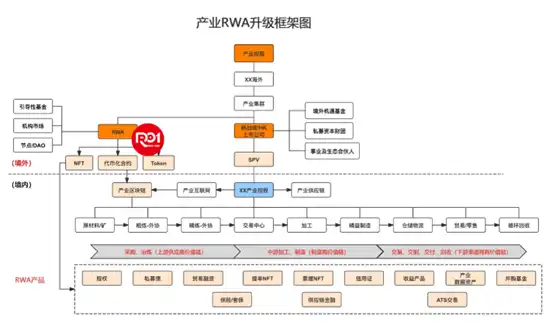

The opportunity points for leading enterprises lie in such an industrial upgrade framework: a distributed underlying asset pool for the industry, RWA assets + transactions/circulation + liquidity, RWA industrial finance, industrial stablecoins, and PayFi. As shown in the diagram:

(Figure Traditional Manufacturing Industry RWA Upgrade Framework)

The advantage of traditional manufacturing lies in heavy assets (underlying assets and fixed assets) and the supply chain. Therefore, the RWA upgrade framework for the traditional manufacturing industry can be divided into four layers:

Layer one, RWA underlying assets, a distributed asset pool, including raw material mine assets, fixed assets, liquid assets, liability-type assets, and more; this involves the tokenization of underlying assets for RWAs, achieving asset on-chain pooling, distributed asset pools, dynamic pricing, etc.

Layer two, industrial chain space + industrial chain scenarios, revolving around the entire manufacturing industry chain of mining processing, international trade, supply chain finance, warehousing logistics, consumption, production, incentive scenarios, as well as core scenarios such as industry chain transactions and liquidity pools, all have opportunities for RWA tokenization.

Layer three, industrial finance (Defi) and industrial stablecoin + PayFI, industrial stablecoins and industrial payment settlement and investment and financing scenarios, as well as encrypted smart finance based on industrial RWA assets for lending, futures, insurance, etc.

The fourth layer, RWA Industry Trading Platform, the upgraded ultimate will inevitably be an industrial RWA trading platform, with exchanges or top-tier exchange's vertical track platform and platform token.

Around traditional industrial upgrades, it will face the transformation issue of digitization and chain-based asset transformation.

This foundational work can simultaneously start with RWA financing to drive infrastructure development, mainly achieving the industry's "controllable assets + trusted asset management," where controllable is for on-chain tradability, deliverability, or control of delivery; trusted asset management involves industrial asset tokenization fundraise management, asset issuance, trading/investment, management, and exit.

For industrial upgrades, for the institutional market, the core is corporate credit, where RWA's controllability and trustworthiness are similar to the on-chain credit mechanism or Oracle mechanism.

Thus: RWA, for a company, is a bond issuance; for an industry, it is a new platform for assets and funds; for a region or country, it is a digital asset, stablecoin, and cryptographic financial system.

#ARAW Always RWA Always Win!

By 2025, the RWA market will rapidly find its place amidst rapid growth. In the new year, Kai will officially start recruiting disciples to mentor and guide. Young talents aspiring to the RWA direction are welcome to take the lead.

More and more friends are coming to ask specific project questions, which cannot be answered in detail on WeChat. A disciple class and practical study camp will be launched soon, so come to the classroom to diligently comprehend, interact, and conduct sandbox scenarios. You can add WeChat YekaiMeta to join the RWA Industry Research Group for discussions.

This article is a contribution and does not represent the views of BlockBeats.

You may also like

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

Should we escape the peak? The principle of the tail-end market in the stock market

RootData: May 2026 Cryptocurrency Exchange Transparency Research Report

Founder of Baixing.com: My Experience with Claude Code in Fourteen Points

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.